Well, mid-February was…interesting here in Texas. As our region, prized for its temperate winter conditions, had its temperatures plunge 50+ degrees below usual, almost to the levels of an Alberta summer, we discovered a few things about our risk management:

People (and businesses) tend to prepare for expected risks, not the infrequent ones – houses here are constructed using electric power and few houses or apartments have gas or wood stoves for heating. Electric companies don’t winterize their operations because “Why spend money to solve a problem that doesn’t exist?” And everyone saves money, until they don’t.

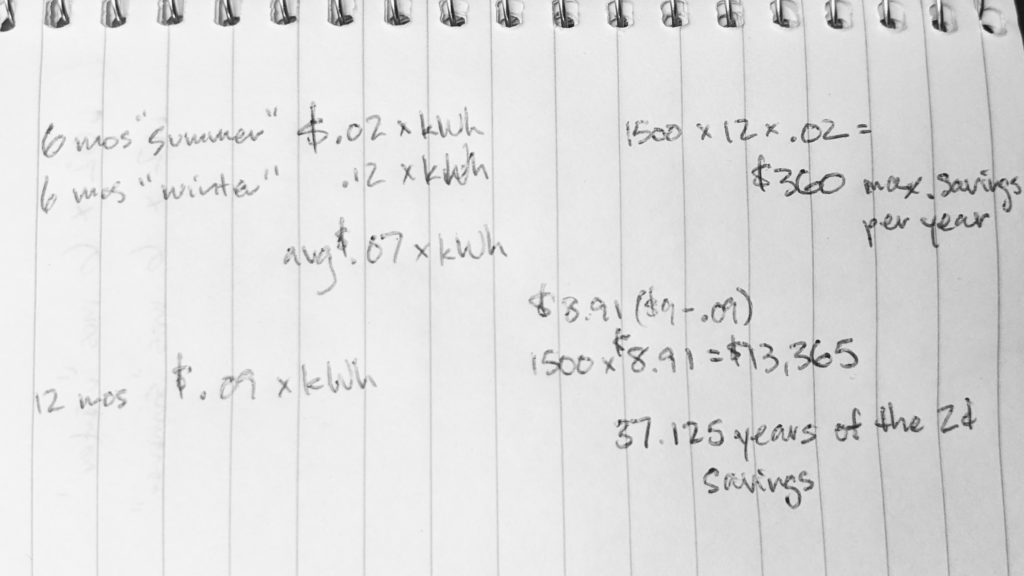

For years, our free market for utilities provided opportunities for competition and models that allowed for companies to sell electricity at variable rates – tacking on a small percentage to the wholesale rate on electricity. With prices as low as 2 cents per kilowatt hour, those variable rates are great…until they aren’t. As demand skyrocketed, the price went from 2 cents to $9/kWh in that week, customers of variable-rate providers like Griddy found themselves getting hit with five-figure electric bills.

Last year, when I was renewing my electric contract, I considered Griddy as a nice way to save money. Overall, though, I opted for a fixed-rate contract at a higher rate – the average savings of a couple of cents per kWh assuming normal conditions weren’t worth the additional risk in my mind.

The whole issue reminded me of some of the times in the rental industry that we’re asked to practice risk management. When we’re trying to calculate if we can handle the big losses that can happen when you chase low prices. Here are a handful:

Insurance

Cut-rate insurance companies are known for providing unbelievably good monthly premiums. Of course, they’re able to do that by not paying or underpaying claims when something does happen, making a bad day worse. (I was going to use a car insurance example here…but sorry, car insurance companies, influencer advertising like this isn’t free.)

Equipment

When I worked at my parents’ rental store, I purchased an off-brand miniature backhoe to save money. The second time it went out, a customer bent the cylinder and the problems kept coming from then on – it spent more time on repair contracts than customer contracts. After two years, I sold for a small fraction of the original price. The short-term cost savings on the front end resulted in a much bigger loss on the sale, on repair costs, and on hacked-off customers disappointed in the quality of equipment they received.

Employees

When you’re hiring, particularly for critical positions, consider the impact the person will have on your company. The $5,000/year you save by selecting the “good enough” candidate may well be dwarfed by the $100,000/year in lost revenue, lost customers, employee turnover, or damaged equipment.

Software

Good software requires constant development. A good software partner is taking advantage of advancements in technology and feedback from users to build enhancements that ensure you’re able to handle everything coming your way. When you’re looking at software, ask yourself the types of questions you’d ask about any other large purchase: Does the software handle maintenance or interface with GPS units so you’re always up-to-date on your equipment servicing? Will it help you out in a lawsuit because it provides customers the necessary operating instructions? Does it bring in more customers by giving you a dynamic online presence? Rental software touches every part of your business – it’s not a great place to take risks.

When you’re looking at vendors, look beyond the up-front price and practice good risk management techniques.